Refractory raw material market spotlighted in Seville

Review of the XII European Congress of Refractory Raw Materials, Machinery & Installation

Graphite | Alumina | Andalusite | Silicon Carbide | Magnesia | Logistics | Decarbonisation | Recycling

Kicking off this year’s European refractory events calendar, Seville in the springtime appeared the perfect place to gather for IMFORMED’s second refractories conference co-organised with ANFRE (Spain’s National Association of Manufacturers of Refractories, Materials and Related Services), the XII European Congress of Refractory Raw Materials, Machinery & Installation, which took place at the Meliá Lebreros, Seville, 13-14 March.

Title Image The spectacular Plaza de España in Seville; Inset top left: Etablissements Gallois SA’s Graphite Mine No. 1, 30km from the port of Tamatave, north-east of Madagascar. From 2018, the operation significantly increased output from 51,000 tonnes to 150,000 tonnes in 2022; Inset bottom left: ANFRE President Julio Mazorra Folguera, formally welcomes delegates.

The conference was preceded by a most convivial networking dinner at the Río Grande Sevilla restaurant, situated alongside the Guadalquivir River.

What our delegates said…

Thanks in organising such a valuable event. It provided a comprehensive platform to discuss the ever-evolving landscape of critical raw materials, volatile market conditions, reliance on Chinese raw materials and the impact of geopolitical tensions on the supply chain

Laxmi Thorat, Director, Minchem Impex FZCO, UAEThank you for the great organisation and kind hospitality. The Congress concluded with a spectacular raw materials panel discussion. I definitely recommend my colleagues to attend this conference next time.

Daria Vitrova, Zaporizhzia Abrasive Plant, Advisor to the CEO, UkraineWe are lucky to have your support, this event was a success with people worldwide.

Eudald Parera, Marketing Manager, Keiron Chemicals sl, SpainI had the opportunity to learn about the European refractory market alongside the major refractory producers and raw materials suppliers. Outstanding organisation.

Marcio Lario, Founder & Board Member, Bautek Minerals Industries, BrazilFree XII Congress Summary Slide Deck Download here

Missed attending the Congress? A full PDF set of presentations available for purchase.

Please contact Ismene Clarke T: +44 (0)7905 771 494 ismene@imformed.com

REVIEW OF PRESENTATIONS

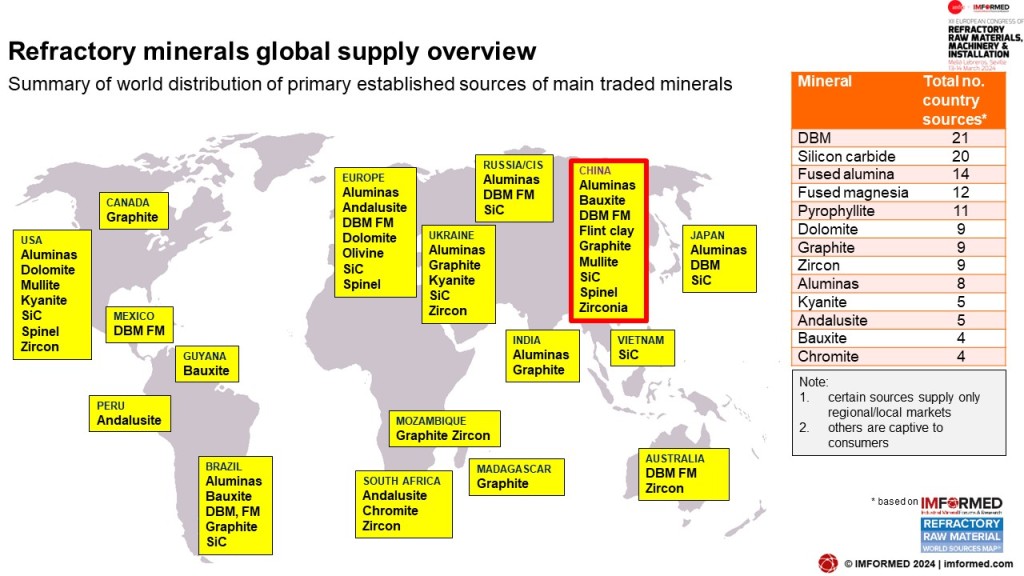

Refractory minerals sourcing & supply overview

Mike O’Driscoll, Director, IMFORMED, UK

A brief review of world refractory minerals sourcing and supply was presented by Mike O’Driscoll, highlighting the global source distribution of refractory minerals, certain of which are relatively limited.

He drew attention to the key influencing factors shaping the supply sector, namely: environment, recycling, costs, limited sources, “criticality”, and China.

Also underlined was the rising awareness across the board (ie. mineral consumers, governments, manufacturing, mainstream media) of the “criticality” of raw materials which will have some, and perhaps positive, ramifications for refractory minerals source and supply development.

Examples given included three announcements in 2023:

- the EU Council’s proposals to improve the Critical Raw Materials Act by raising the level of recycling capacity from 15% to 20% (ie. 20% of the EU’s annual CRM consumption from recycling), and adding bauxite and alumina as strategic raw and critical materials

- the US DoE Critical Minerals List Update 2023, which added natural graphite and silicon carbide

- and in December 2023, China’s Ministry of Commerce & Customs set export controls on natural flake graphite and its products, high purity synthetic graphite and its products, including spherical graphite; which will assist growth potential in new ex-China sources in Africa, North America, and Australia

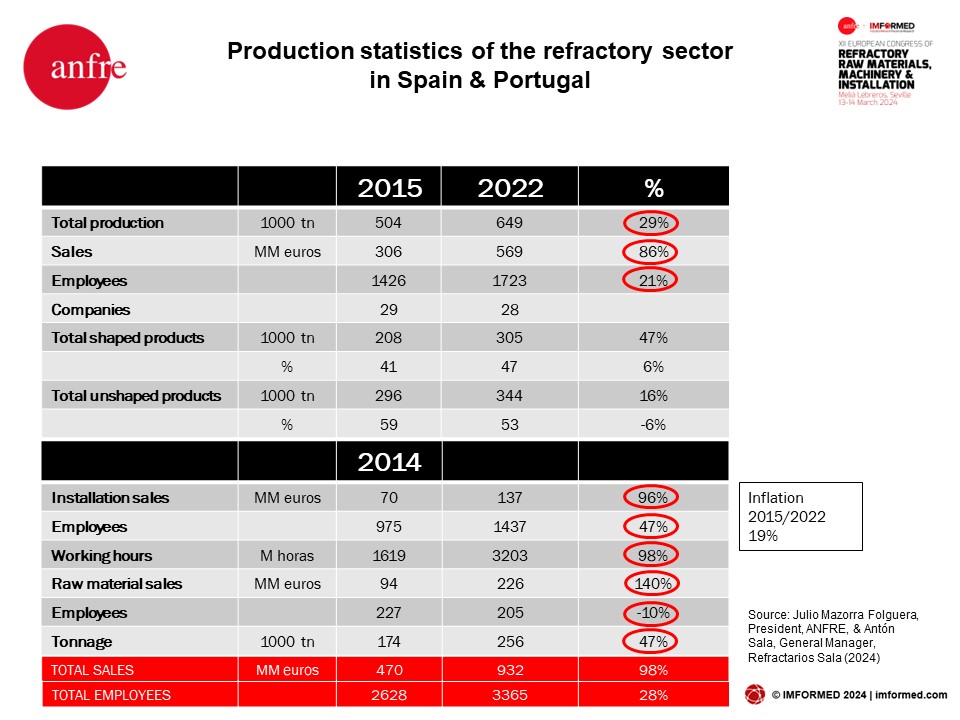

Production statistics of the refractory sector in Spain & Portugal

Julio Mazorra Folguera, President, ANFRE, & Antón Sala, General Manager, Refractarios Sala, Spain

ANFRE President Julio Mazorra Folguera, formally welcomed delegates to the congress before presenting a review of key statistics of Spain and Portugal’s refractory industry.

Notable figures included an increase in production since 2015 of 29% to 649,000 tonnes in 2022, with shaped products accounting for 47% and unshaped products 53%.

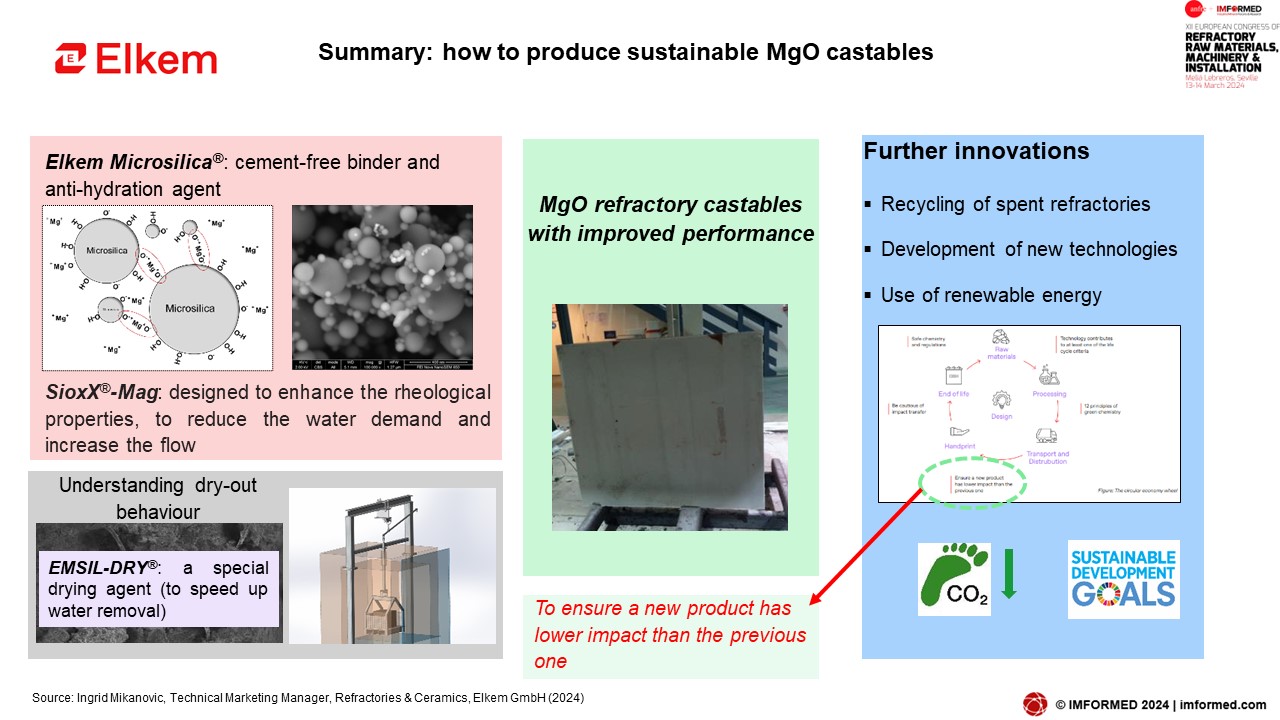

Developing sustainable cement-free magnesia castables

Ingrid Mikanovic, Technical Marketing Manager, Refractories & Ceramics, Elkem, Germany

The industry is aiming for long life, low consumption, energy saving, low carbon foot-print and recyclability.

Elkem’s objectives are to develop a more sustainable crack-free MgO castable by controlling hydration and drying behaviour.

Mikanovic explained how microsilica plays an essential role as an anti-hydration agent for MgO. The dosage of microsilica and the size of MgO in the castable all have a strong impact on crack formation during both the curing and dry out processes.

The Macro-TGA has become a unique tool to facilitate design of an optimised heating profile. By using a combination of microsilica (to protect MgO from hydration), a speciality drying agent (to speed up water removal) and optimum dry out profile, magnesia castables based on the MgO-SiO2-H2O bond system have been successfully developed.

Nevertheless, it is not an easy task to produce MgO castable at an industrial scale. More work is needed. Therefore, several approaches could be taken in order to ensure that a new product has a lower CO2 impact.

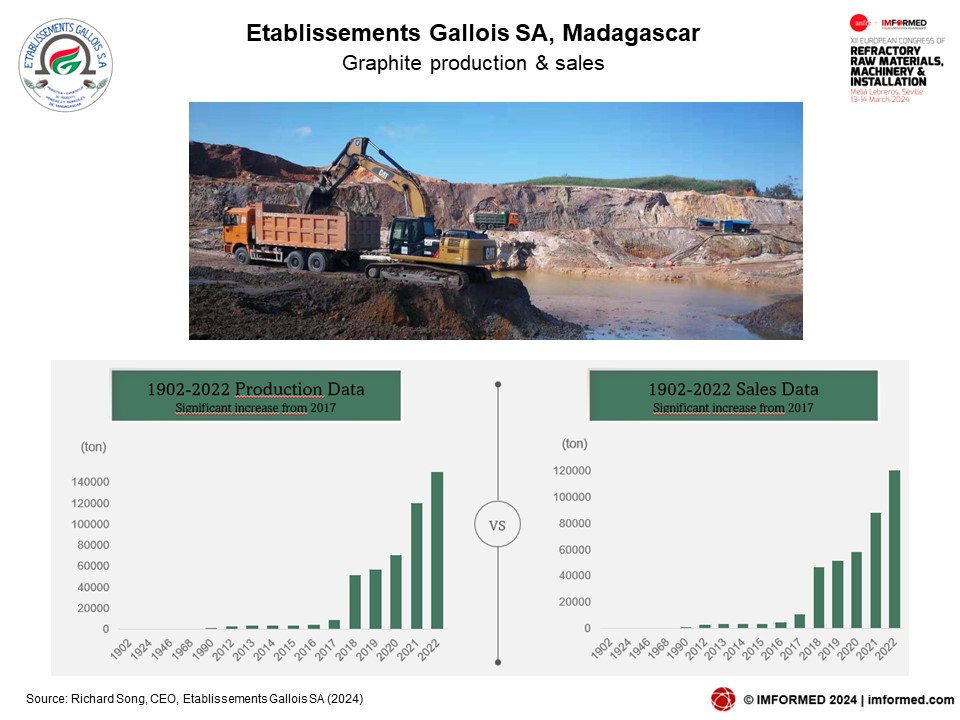

Global graphite market analysis & Gallois Graphite Madagascar

Richard Song, CEO, Etablissements Gallois SA, Madagascar

Richard Song provided an excellent summary of the global graphite market followed by an update of the operations of Gallois Graphite Madagascar.

Song reminded of the recent enactment of controls on Chinese graphite exports and its impact, noting the spike in graphite exports in November 2023 (23,503 tonnes) and then sharply dropping in December 2023 (1,428 tonnes).

Obtaining an export license for graphite is linked to many uncertainties, and it is apparently relatively easy to get licenses for smaller quantities <100 tonnes. No export licenses have been issued for graphite export to India so far.

The rapid development of electric vehicles has boosted the fast-increasing demand of anode materials, in particular graphite, the primary choice for lithium ion batteries.

Owing to falling domestic demand, prices for natural graphite have bottomed and most graphite companies in China suffered losses in 2023, with many closing.

However, China is short of large flake graphite, with about 50% of domestic demand needing to be imported to mainly produce expandable graphite.

This shortfall has increased the production and blending of so called man-made flakes or “fake flakes”, ie. smaller particles are pressed together to form larger particles. Blending with fake flakes can significantly reduce the performance of the graphite, thus consumers are now wary of Chinese flake graphite grades.

Located in the north-east of Madagascar, in the province of Tamatave, Gallois’ mine has an estimated 240m tonnes of graphite reserves. From 2018, the operation significantly increased output from 51,000 tonnes to 150,000 tonnes in 2022.

In 2023, the company installed a new high purity and expandable graphite production line with an output of 30,000 tpa. By 2030, Gallois plans to have a production capacity of 200,000 tpa natural graphite, and 200,000 tpa synthetic graphite.

What’s happening in China? The best place to find out…

Field Trip to Haimag Magnesite, Haicheng Thursday 24 October – Full Details here

ECO-TAB® alumina refractory aggregate for steel ladle lining

Dr Sebastian Klaus, Technical Manager Europe, Almatis GmbH, Germany

Klaus started by describing energy losses in steel ladles and the effect of refractory weight when the crane in a limiting factor.

Almatis, a global leader in speciality alumina materials, has developed ECO-TAB® – a lower-density alumina refractory aggregate designed for wear linings.

Experimental ECO-TAB® recipes in castables were explained and the key advantageous properties outlined, along with results of corrosion resistance in a slag test in an induction furnace.

Key benefits using this new alumina material include:

- energy saving by reduced heat capacity and thermal conductivity in in processes with thermal cycling (eg. steel and foundry ladles)

- strong thermomechanical stability and wear resistance

- reduced weight of refractory linings

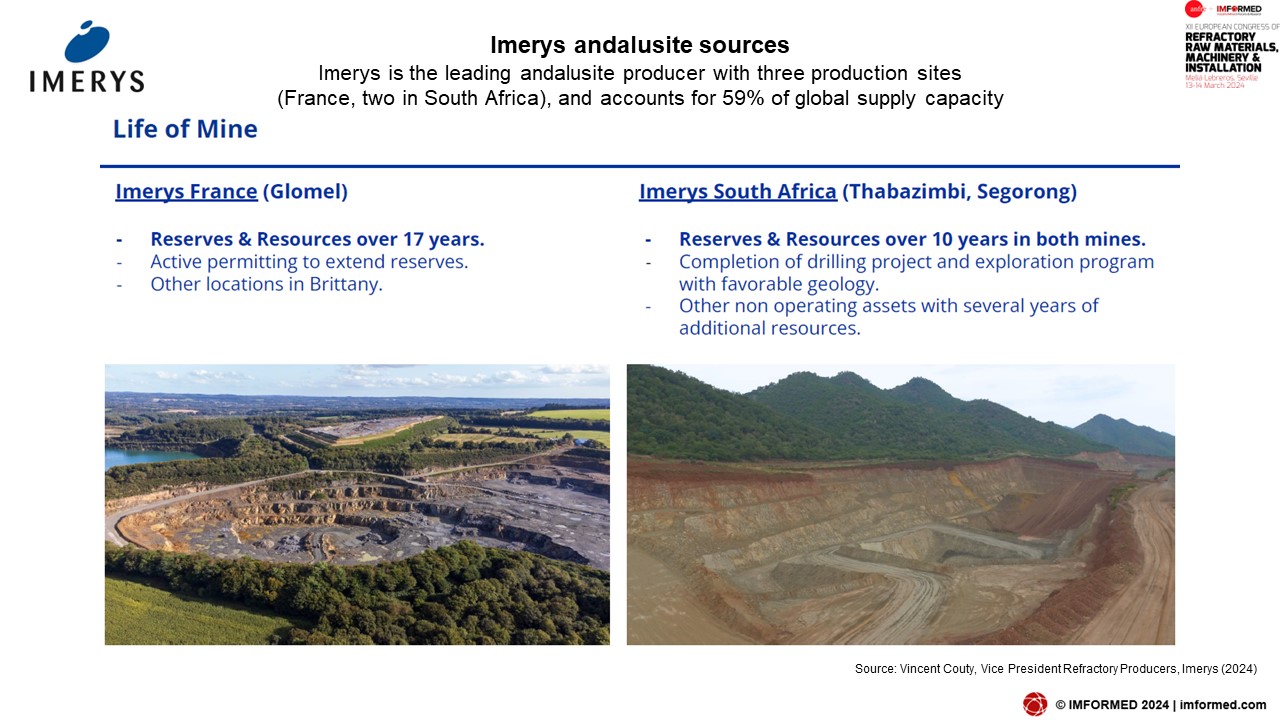

Andalusite supply & demand for refractories

Vincent Couty, Vice President Refractory Producers, Imerys, France

Couty’s presentation covered andalusite’s unique characteristics, applications in refractories, global demand drivers, supply capacity, challenges of operating in South Africa, actions to improve service level, Imerys’s product range and sustainability roadmap.

Andalusite features a good compromise and imparts interesting properties such as: resistance to thermal shock, high refractoriness under load and creep resistance, coarse crystal size compared to sillimanite and kyanite, limited porosity (single crystal), and in situ mullitisation compared to preformed mullite containing raw materials.

Global market demand is about 260,000 tonnes with an annual growth of +2% to +6%. Proximity to market and relative cost position impacts the use of andalusite in refractory formulations, with South Africa and Europe being the largest volume use markets.

Couty noted growing demand in India from steel production increases projected at +8% pa.

There is underdevelopment in China owing to technological maturity, profitability constraints, and availability of lower priced material (refractory grade bauxite). However, this is changing and market penetration is increasing with the shift of steelmakers’ business models from cost to efficiency, and a mid-term shortage of refractory bauxite.

Imerys is the leading andalusite producer with three production sites (France, two in South Africa), and accounting for 59% of global supply capacity, the other players being ARM Andalusite in South Africa, Andalucita in Peru, and Chinese players.

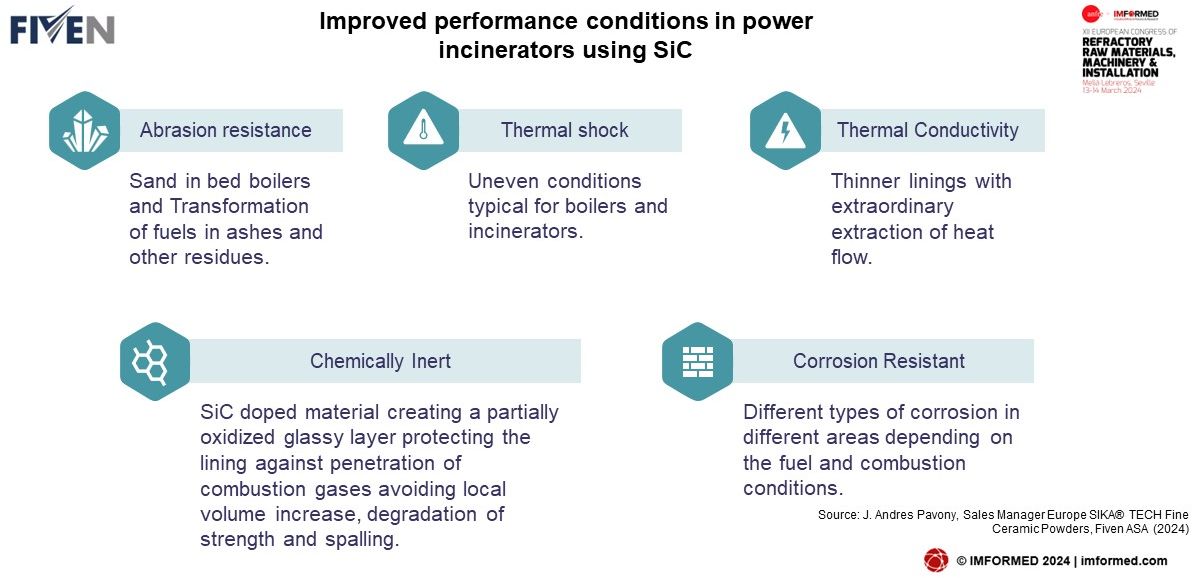

Silicon carbide solutions for refractory applications

J. Andres Pavony, Sales Manager Europe SIKA® TECH Fine Ceramic Powders, Fiven ASA, Germany

Pavony highlighted the main attributes of silicon carbide’s use in refractories, such as its harness, chemical inertness, high thermal shock resistance, low thermal expansion, and high thermal conductivity.

Fiven, acquired by OpenGate Capital from Saint-Gobain in 2019, is headquartered in Oslo, operates four SiC production sites, and has grades ranging from <90% – 98% SiC.

Pavony outlined how Fiven’s Waste to Energy (WtE) aligns with EU energy and climate policy, optimising waste management while contributing to energy efficiency goals, providing a preferable alternative to landfilling.

The talk concluded with an illustration of how silicon carbide improves performance conditions in power incinerators.

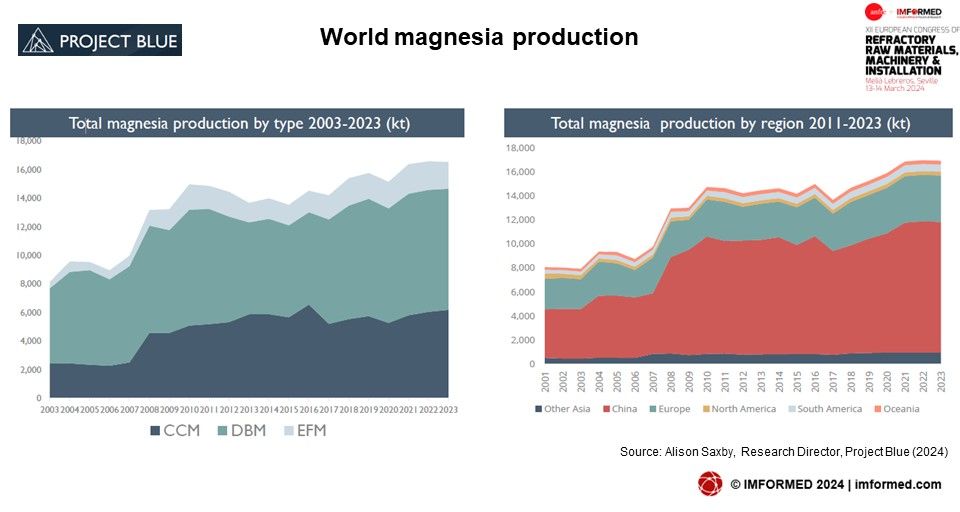

Magnesia supply overview

Alison Saxby, Research Director, Project Blue, UK

Saxby set the scene by covering the types of magnesia and sources, magnesite ore – shifting patterns, supply of refractory materials, dead burned magnesia supply, high grade magnesia supply, fused magnesia supply, global trade, and the key narratives in the industry.

China dominates Asian supply, there were lower levels of supply from 2018, firstly due to mining restrictions and increased environmental regulation, and subsequently coupled with reduced activity due to Covid.

Within Europe, Turkish production has increased significantly over the last ten years, and Russia is the other country with significant capacity – both Kumas Manyezit and Magnezit have expanded their mining operations in recent years – but with decreased export activity Russian output has been adjusted accordingly.

Saxby noted that there has been change in Chinese magnesia production over the last five years, as the industry adapts to:

- Tighter regulations and environmental controls

- Consolidation in the industry

- Move to higher quality refractory production – increasing domestic EFM and HG DBM production

- Long term government strategies to protect the industry, including a reduction in production from Liaoning

While magnesia refractories are playing a key role with a move to more EAF in steelmaking, any potential and emerging new magnesia supply players outside China face real barriers to entry, such as raising capital and permitting new operations.

The latest trends in magnesia markets? Find out here…

EARLY BIRD RATES END MONDAY 1 APRIL!

Field Trip to Grecian Magnesite, Yerakini, Thursday 16 May – Full Details here

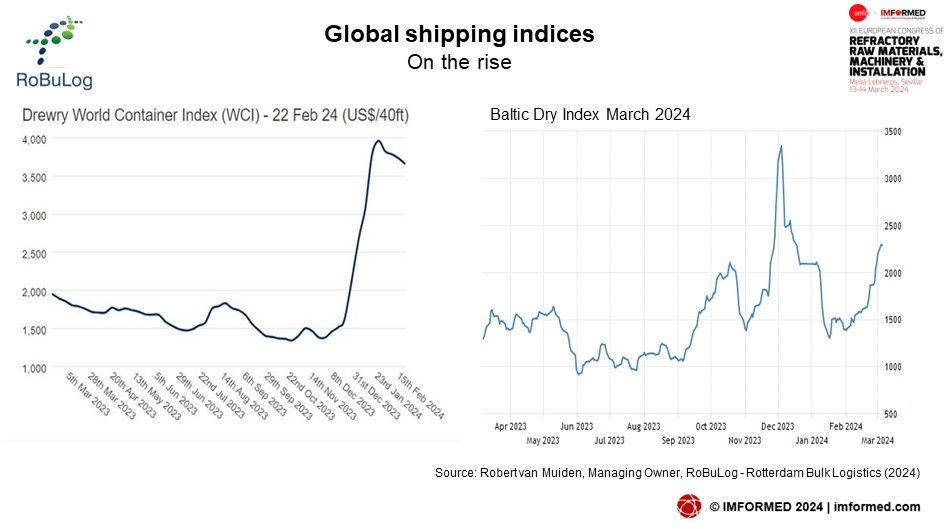

Status & outlook for mineral logistics

Robert van Muiden, Managing Owner, RoBuLog – Rotterdam Bulk Logistics, the Netherlands

Van Muiden focused on global and European issues of the logistics market which is very much the jugular of refractory mineral supply chains.

He explained how the aftermath of the Suez blockade and the two “lost” years of Covid-19 is still felt globally today in the shipping business.

More recently, the energy price surge following Russia’s invasion of Ukraine resulted in the EU and USA concluding that they are depending too much on external resources, like Russian gas or Chinese rare earths, and also refractory minerals.

They have each lined up high financial support schemes to mitigate this, and this will also impact on logistics & shipping.

Also, the Houthi threat on Red Sea shipping has added to costs and journey times as voyages are redirected around the Cape of Good Hope.

All this impacted container freight first, followed by the dry bulk market. Now, the latter is being affected by vessel supply, low investments in new fleet, energy regulations, and economic uncertainty.

In Europe, the lowering of water levels in the Rhine have significantly impacted shipping via this vital artery.

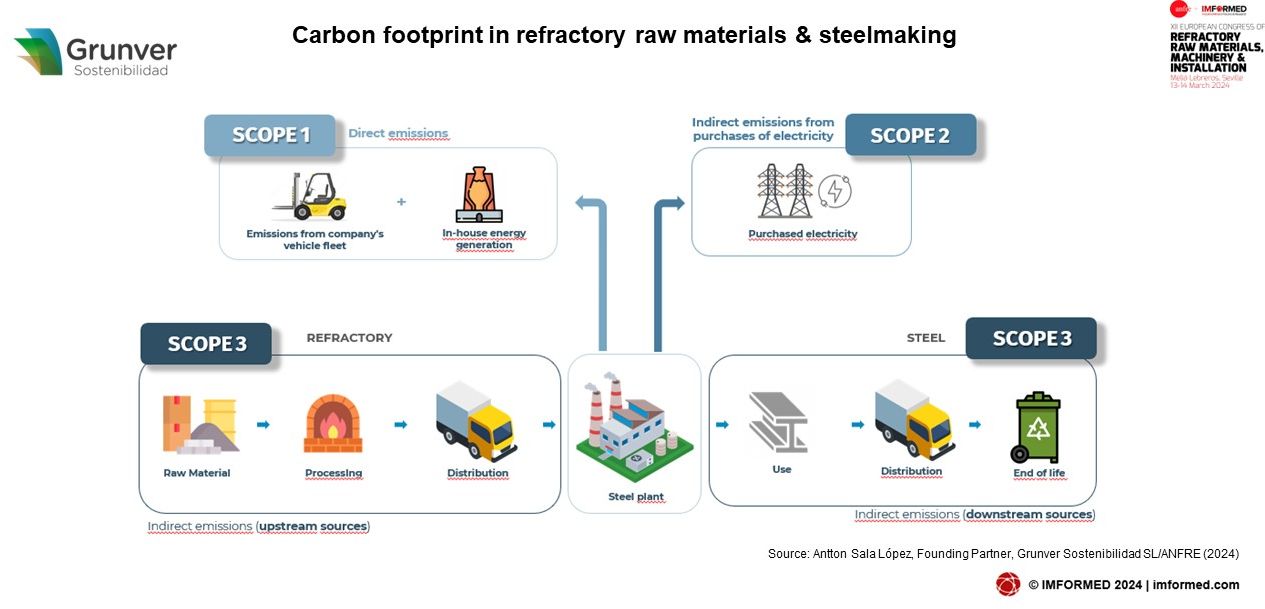

Decarbonisation with Life Cycle Thinking: Refractory raw materials & their relevance

Antton Sala López, Founding Partner, Grunver Sostenibilidad SL/ANFRE, Spain

Sala started by explaining the context of Life Cycle Thinking and Life Cycle Sustainability Assessment-based tools, followed by a closer look at the carbon footprint and its context, emission sources, and relevance, before concluding with a refractory raw materials project developed for ANFRE by Grunver Sostenibilidad.

Carbon Footprint Scopes 1-3 were clarified, and usefully highlighted in the context of refractory raw material production and steel production.

Sala drew attention to Scope 3 (indirect emissions, upstream sources) and the role of refractories in this area. Although Scopes 1 and 2 are already highly controlled by companies, Scope 3 is one of the main touchstones of climate change management.

Recently, organisations have become more aware that the majority of their value chain’s carbon footprint is associated with Scope 3 emissions (some data suggests that Scope 3 emissions can be up to 4 times the emissions of Scopes 1 and 2).

Grunver Sostenibilidad has provided a series of emission factors for raw materials used in refractory manufacturing processes for ANFRE with the objective of integrating emission factors into product or organisation carbon footprints, facilitating supply chain assessment (Scope 3).

Circular economy: demolishing used furnaces & recycling of refractories

Werner Odreitz, CEO, REF Minerals GmbH, Germany

Odreitz demonstrated how REF Minerals was “ahead of time” in its operational ability, refractory raw material selection, and its certification in recycling refractories.

REF Minerals’ core activity has been the recycling of spent refractories from glass furnaces, and so the main minerals handled are zircon, zirconia, AZS, alumina-chrome, alumina, chrome oxide, and magnesia.

The company was founded in Riga, Latvia in 1997 to trade secondary raw materials, and a first processing plant was built in 2012 where incoming materials are cleaned, hand sorted, graded, sized, packed and distributed.

In 2016, a patented treatment plant to reduce Cr VI (hexavalent chrome) was built and operations started, and REF Minerals GmbH was relocated to Düsseldorf.

In 2022, the Czech demolition company SEBOREF s.r.o was acquired, which specialises in demolition of glass and glass fibre aggregates. In 2023 a second processing plant was under construction in Dolní Rychnov, Czech Republic.

Refractory recycling trends & developments, all you need to know…

Speakers from Glenn Hunter, RHI Magnesita, MIRECO, REF Minerals, TRL Krosaki, Shinagawa, HarbisonWalker International, Lhoist – Full details here

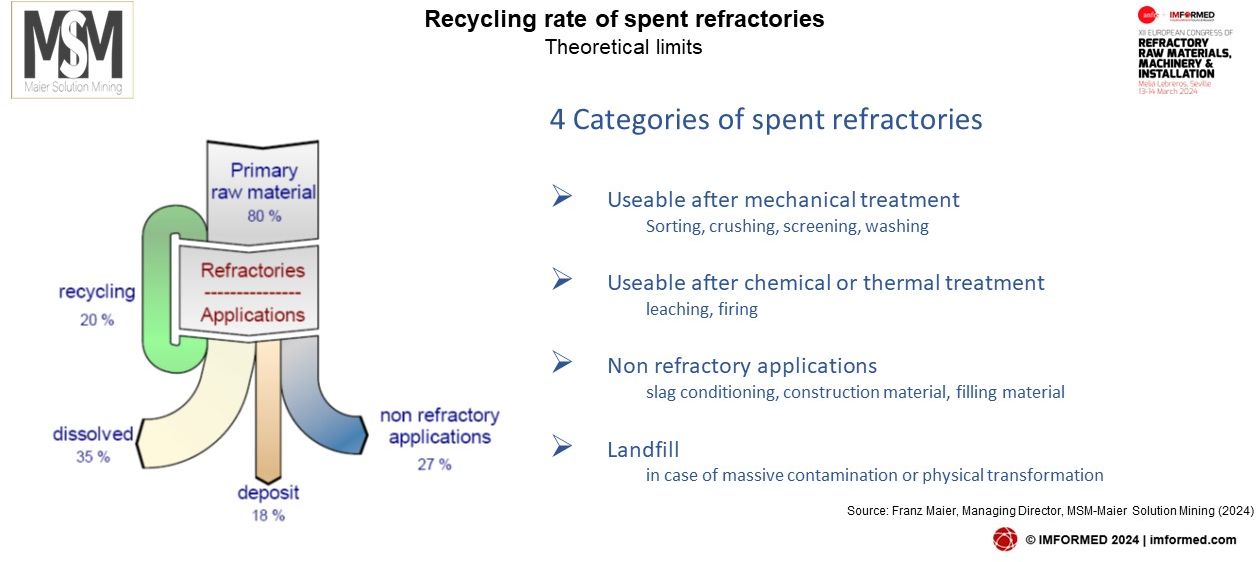

Recycling of refractories: nice to do or a need to have?

Franz Maier, Managing Director, MSM-Maier Solution Mining, Austria

Meier concluded the presentations with a thought provoking reality check on the state of refractory recycling, in particular putting it into perspective and asking who should be accountable for what, and even if at all.

He covered the EU Green Deal, the part of the Circular Economy in the Green Deal, examples of direct and indirect impact, and recycling of refractories.

While there are very good reasons for refractory recycling, Meier highlighted the main obstacles:

- Refractory break out is classified as waste

- Material loss during usage, structural or chemical modification, infiltration

- Huge variety of products – Different qualities and shapes

- Big differences in lifespan leads to difficulties in constant supply

- High bureaucratic burden for cross boarder shipment of spent refractories

- Different waste regulations in European Member States

- Acceptance from customers

He suggested some recommendations to boost refractory recycling:

- Decrease of bureaucracy

- Harmonized European Waste Regulation

- Easing of the End of Waste classification

- Circular Economy obligations for Customers

- Product design for easier selective breakout

- Customised sourcing according lifespan of the application

- Higher stockpiles to guarantee constant quality of the secondary raw material

- Acceptance from customers

Discussion on these points among other hot topics continued in a lively Raw Materials Discussion Panel involving refractory experts and delegates. Among the comments was a call for the refractory industry to undertake action to present some kind of unified front for the progression of decarbonisation methods and goals across the industry.