Dic 16

China’s magnesia prices static in quiet post-holiday market

China’s magnesia market has showed no changes in the first week after the Lunar New Year, with prices holding at current levels while more market players are yet to return from holiday this week.

China’s magnesia prices held steady after the holiday amid thin spot buying, while market logistics gradually began to recover this week and more buyers are away and not due to return until after the Lantern Festival on February 19.

Domestic prices remained soft this week due to weak demand from downstream buyers, though some producers have already resumed production and others will resume production next week.

«Our factory hasn’t resumed production this week as most workers haven’t returned from holiday. The market is quiet in both the domestic and export sectors and there are no changes on the spot market. [Ship and truck] cargo transportation has just started to recover as well,» a producer told Fastmarkets IM.

China’s magnesia market has been pressured by continuous mining restrictions and the prohibition of explosives due to stricter environmental regulations in Liaoning province over 2018, which have continued into 2019. There has been speculation on whether China’s government will remove the explosives ban in the first half of 2019, but currently no further news has been reported.

«We haven’t started new purchases this week because we are fresh back from holidays, and we still hold a watchful attitude toward the market. If the government re-permits explosives on magnesite mining this year, I think prices will have some downtrend potential,» a buyer said.

Fastmarkets IM’s assessment of the fused magnesia (FM) 97% MgO (Ca:Si 1:1) price was at $950-1,050 per tonne fob China on February 12, unchanged week on week.

While the Fastmarkets IM assessment of the price for the FM 97% MgO (Ca:Si 2:1) market was at $1,200-1,300 per tonne on Tuesday February 12, also stable with the previous week.

The price assessment for the dead-burned magnesia (DBM) 90% MgO lump market was at $230-260 per tonne fob China on February 12, also flat with the previous week.

Dic 10

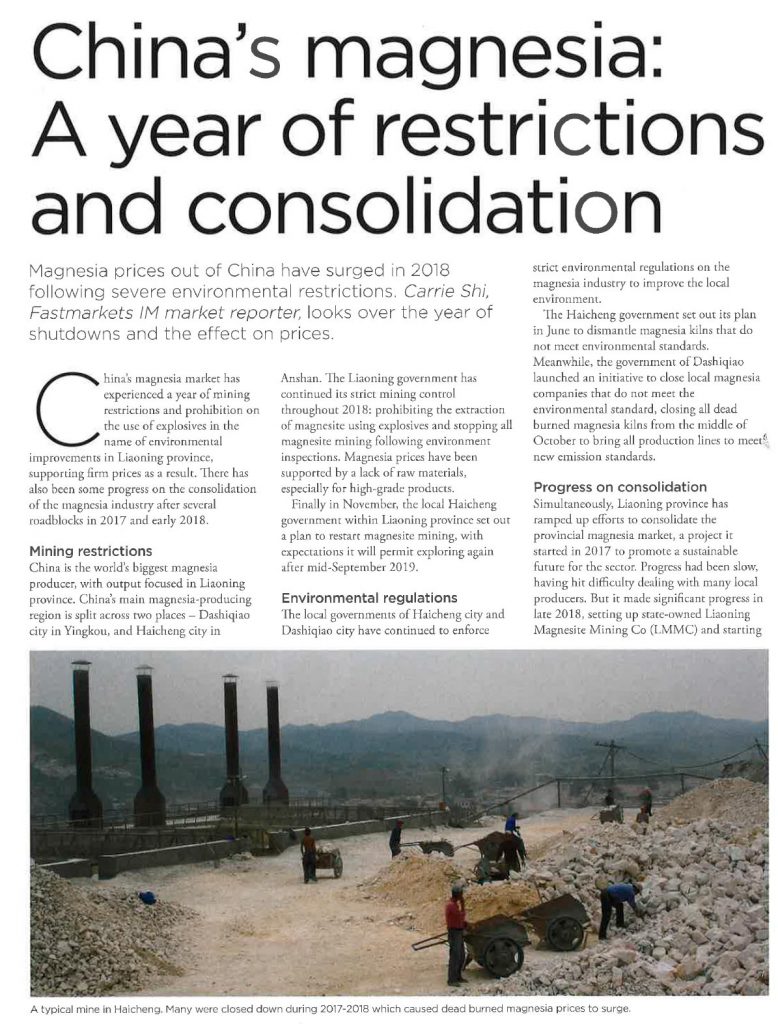

China’s magnesia: A year of restrictions and consolidation

Magnesia prices out of China have surged in 2018 following severe environmental restrictions. Carrie Shi, Fastmarkets IM market reporter, looks over the year of shutdowns and the effect on prices.

![]()

Dic 02

Low demand, inconsistent supply keep bauxite market weak

Prices for two grades of bauxite have ticked downward, as has the price for white fused alumina, but brown fused alumina remained stable, with the market said to be mostly flat on limited activity.

The markets for both bauxite and alumina continued to be weak in early March on slow demand flows in Europe and other consuming areas, while the evolution of the supply situation in China remained unclear.

Fastmarkets assessed the price of calcined bauxite, 85%, at $400-420 per tonne fob China on Thursday March 7, against $410-430 per tonne previously.

The corresponding price assessment for calcined bauxite, 86%, was $420-440 per tonne fob China on the same day, down from $430-450 per tonne earlier.

Fastmarkets’ price assessment for calcined bauxite, 87%, remained unchanged on Thursday at $450-470 per tonne fob China, while the price ofcalcined bauxite, 88%, remained at $470-490 per tonne fob China. The prices for 87% and 88% material dropped by $20-30 per tonne in the previous assessments on February 21.

Market participants spoke of widespread weakness across the market at the moment, especially on the demand side.

The majority of consumers had contracted their supplies in advance for the first part of the year, and many were covered for most of the first half. The slowdown in European industrial indicators, visible since the third and fourth quarters of 2018, also played a part in damping market activity.

As a result, the industry was not taken by surprise by the current weakness.

A number of sources noted, however, that the slowdown has gone further than expected.

«We all knew that this year was going to be slower than 2018, so it’s not necessarily a surprise,» one importer said.

What is notable, though, is that the drop in inquiries has been more significant than we forecast.»

A producer added: «There may have been some excess of optimism on the part of customers at the end of last year. Business has slowed more than expected.»

Nov 25

Perspectives for Synthetic Aluminas in the Refractories Market

At present, the raw materials market for the refractories sector is very dynamic. We approached Almatis, who is a well known global player in the alumina business. Emre Timurkan (ET), CEO Almantis, was prepared to share with our readers his views. Emre Timurkan has over 20 years experience in the financial markets, having worked in commercial and investment banks globally. Joing Oyak, Turkey’s largest pension fund in 2017, he was appointed CEO of Almatis in August 2017. Emre Timurkan also serves as a Member of the Oyak Executive Committee, Deputy Chairman of Oyak Anker Bank, and Member of the Board of Oyak Global Investments. He is a graduate of Georgetown University in Washington DC/US with a BSBA in Finance.