See article below from the April issue of Industrial Minerals magazine, for market updates on price movements in various industrial minerals. Minerals featured this month include: magnesia, titanium dioxide, chromite, graphite, zircon, lithium and andalusite.

IM’s full price listing is only published online. If you have any comments or concerns, or wish to discuss any of the grades or prices listed, please contact Barbara O’Donovan, Industrial Minerals editor bodonovan@indmin.com. Magnesia Weak demand weighs on Chinese magnesia market The prices for all grades of China-origin magnesia assessed by Industrial Minerals remained unchanged at the beginning of March in response to limited buying interest.

Overseas consumers had no immediate need to purchase and were waiting for clarity in the market, although high-grade magnesia products remained in tight supply because of a lack of high-quality raw materials. Industrial Minerals’ assessments of the prices for dead-burned magnesia (DBM) products remained stable.

The fob China price of DBM 90% MgO lump was $240-280 per tonne on Tuesday March 13, while 92% MgO material was priced $280-300 per tonne, both unchanged from the previous week.

Mid-grade magnesia 94-95% MgO prices were stable at $680-700 per tonne fob China while the price of 97.5% MgO material remained at $1,100-1,400 per tonne fob China.

«Supply of high-purity magnesia 97.5% MgO remained tight, and only a few producers can produce materials which guarantee the content of MgO reaching 97-97.5% because the government still exerts strict control on [the use of] explosives [in mining]. But trading activity remains slow this week,» a Dalian trader told Industrial Minerals.

«We have stopped signing long-term contracts with overseas buyers because of a lack of sufficient magnesia stocks, and negotiate prices with buyers according to each order currently,» a producer in Haicheng said. «One magnesia company in Haicheng had an accident with a gas poisoning, and most Haicheng magnesia producers have halted production for safety inspections,» he added.

«But this accident will have a limited effect on magnesia prices because of current weak demand from downstream consumers.» The markets for fused magnesia (FM) and caustic calcined magnesia (CCM) were flat the week of March 13, with prices unchanged.

Overseas buyers were in no hurry to buy and submitted lower bids in an attempt to push prices downward. The spot price of FM 97% MgO (Ca:Si 1:1) remained at $1,150-1,250 per tonne fob China on March 13, while the price of 97% MgO (Ca:Si 2:1) was stable at $1,250-1,400 per tonne.

«I received a bid at $1,100-1,150 per tonne for FM 97% MgO (Ca:Si 2:1) from an overseas customer this week, which was too low to accept because current prices are above $1,250 per tonne on the spot market,» a trader in Dalian told Industrial Minerals.

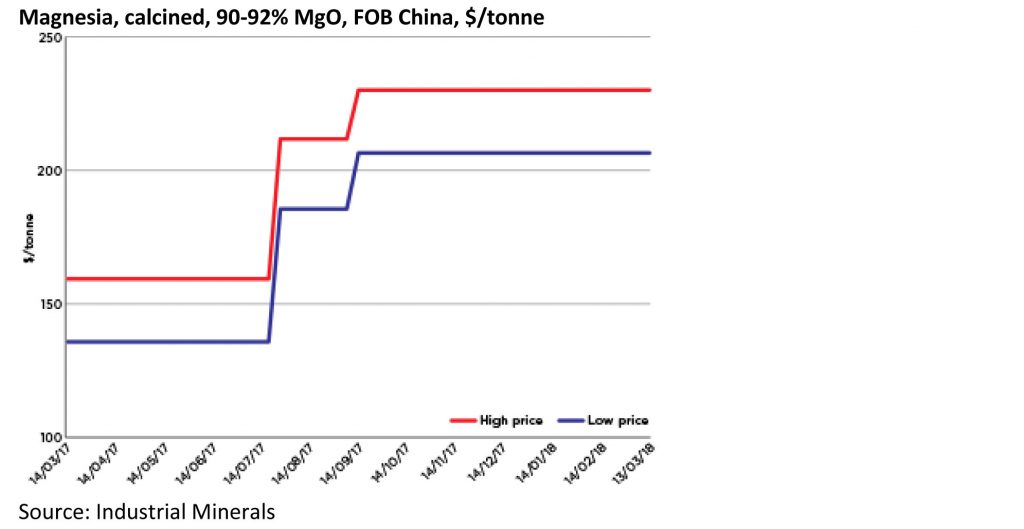

The fob China prices for CCM materials held steady at $205-230 per tonne for 90-92% MgO, $240- 260 per tonne for 94% MgO, and $335-355 per tonne for 96% MgO. «Because of the lack of high-quality magnesite, we do not have high-grade CCM 94% and 96% [available for sale] now,» a trader in Dalian said. «CCM 90-92% MgO prices were stable, but demand hasn’t picked up.»

Graphite Chinese flake graphite prices stable on slow demand Flake graphite prices in China have been stable recently, with downstream buyers showing no interest in stocking materials because the first quarter of the year is usually the slack season.

«Prices haven’t fluctuated and are unchanged. Overseas buyers usually start to purchase from the second quarter of each year, and I expect there to be more deals next month,» one producer in Qingdao told Industrial Minerals.

«I have heard there will be another round of environmental inspections in Shandong, and some companies will start the project of changing [their] fuel [source] from coal, which might tighten supply and push prices higher at a later date, but there is no precise news at the moment,» he added. According to Industrial Minerals’ price assessment on Thursday March 15, prices for flake graphite, 94-97% C, +100 mesh, on an fob China basis, were stable at $800-940 per tonne, in line with stable Chinese domestic prices.

The price for +80 mesh material of the same carbon content was $1,050- 1,210 per tonne, also unchanged from the previous week. The prices of other grades, including 85-87% C +100 mesh and 90% C -100 mesh, remained unchanged at $590-620 per tonne and $600-650 per tonne fob China, respectively. The price of flake graphite, 94-97% C, -100 mesh, was assessed at $655-790 per tonne.

«The flake graphite market is quiet, with prices stable because of the limited orders from buyers. While some suppliers with positive outlooks are keeping their offers firm for spherical graphite in the domestic market, at 17,000-20,000 yuan [$2,686-3,160] per tonne, buyers are not active in purchasing at the moment, and we haven’t started to adjust our export prices on thin buying activity,» another producer in Qingdao said.

Industrial Minerals’ assessment of the price for spherical graphite, 99.95% C, 15 microns, was steady at $2,250-2,700 per tonne fob China on March 15. Zircon Zircon buyers mull substitution amid Q2 price increases Zircon prices are likely to rise in the second quarter of 2018, traders, suppliers and end-users have predicted. Richards Bay Minerals (RBM) has informed customers that it is raising its price for zircon to $1,500 per tonne from $1,200 per tonne previously, effective from April 1, multiple market participants have told Industrial Minerals.

RBM, which has not publicly announced the rise, declined to comment when contacted by Industrial Minerals. This comes after Iluka said that its zircon reference price will rise to $1,410 per tonne for the six months beginning on April 1. Its reference price had been $1,230 per tonne since October 1 last year. In effect, Iluka’s prices will range from $1,410 to $1,480 per tonne from the start of next month, sources said.

There is generally no discount for larger volumes, they added. While negotiations by companies that have yet to announce their second-quarter prices will continue until the end of March, market participants predicted that zircon prices from all producers will range from $1,410 to $1,600 per tonne, depending on the producer and the country of origin.

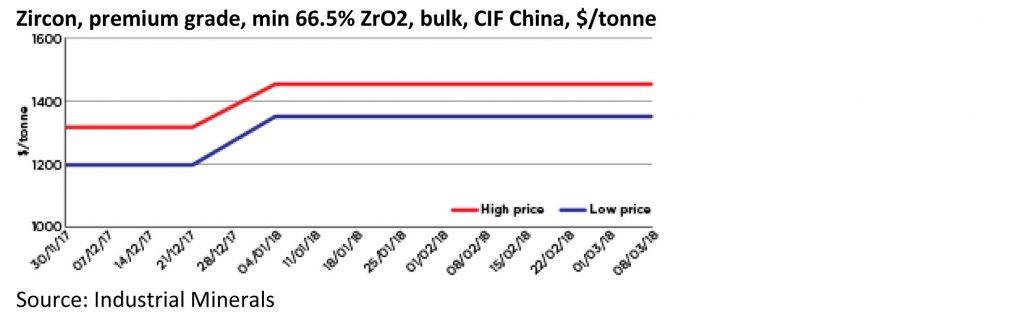

Industrial Minerals assessed prices of zircon, premium grade, min 66.5% ZrO2, bulk, cif China at $1,350-1,450 per tonne on Thursday March 8, unchanged week on week but up from $1,200-1,320 per tonne in December. Market observers and participants attributed the price rise largely to reduced supply – but both high prices and a lack of available material raise the risk of zircon being substituted by another material.

End-users in the refractories and ceramics markets may switch to alumina to secure supply at a lower cost, for example. Alumina is cheaper, its price is more stable and supply is easier to secure. The price of alumina, calcined, ground 98.5-99.5% Al2O3, bulk, ex-works US/Europe, long-term contract, is $830-930 per tonne, for example. «Some companies are thinking of substitutes» and, while the end-of-year price picture is uncertain, substitution of zircon would «not be good for the sector» because it would be an irreversible change, an end-user in Europe said. The threat of substitution is greater in zirconia rather than in zircon or zirconium, «considering its price [which is two to three times the price of the raw material] and the high degree of competition,» another zircon processor in Europe said. «Any substitution of zircon with alumina threatens to be a permanent change.»

Global supply of zircon is unlikely to increase until 2020 or 2021 unless Indonesian miners boost their production, one market participant told Industrial Minerals. Substitution was evident in 2011-12 when prices rose to high levels. Premium-grade zircon prices were higher than $1,500 per tonne during that period, with Iluka Resources reportedly selling material for more than $2,000 per tonne before dropping its price to $1,885 per tonne in October 2011 and Rio Tinto offering premium-grade zircon in a range of $1,800- 2,000 per tonne.

Prices tumbled from this peak when consumption fell in the ceramics and foundries end-markets – users turned to alternative materials such as alumina at that time. In many cases, zircon consumers were unable to pass on increased costs, particularly in the ceramics market. «Miners must be conservative on [price] increases,» the end-user added.

Zircon Kenmare expects to see zircon prices increasing in 2018 Mineral sands miner Kenmare has reported record mineral sand production in 2017 and has forecast rising prices for ilmenite and zircon this year.

On March 4, the Ireland-based miner reported that its 2017 ilmenite production had gone up by 11% year-on-year to 998,200 tonnes, while zircon production increased by 9% to 74,000 tonnes.

The company reported revenues for Kenmare Resources of $208 million for 2017, up by 47% yearon-year, on the rise in prices for mineral sands. «Global markets for our products improved strongly in 2017, continuing the market recovery experienced in 2016,» Kenmare said.

«Inventories of titanium feedstocks and zircon, which had been high for several years, declined below normal operating levels during 2017, supporting long-awaited product price increases.»

Industrial Minerals assessed the price of zircon, premium grade, min 66.5% ZrO2, bulk, cif China at $1,350-1,450 per tonne on January 4 this year, compared with $1,030-1,100 per tonne a year earlier. The assessment on March 8 showed that the price has not changed since January.

«Ilmenite prices continued to rise through 2017, albeit at a slower rate in the second half of the year, as low-grade concentrates were introduced into the market and Chinese environmental inspections caused disruption,» Kenmare managing director Michael Carvill said.

«Received prices are expected to average at higher levels in 2018, supported by continued demand growth and a reduction [in the amount] of low-quality ilmenite supplied from stockpiles,» he added. He was even more bullish on zircon prices.

«The zircon market remains tightly supplied, with strong price increases throughout 2017 and significant further rises already in 2018,» he said.

«Zircon prices remain far below the peaks achieved in 2012,» Carvill noted, although he added that «tight supply conditions are expected to continue and may lead to some thrifting and substitution.»

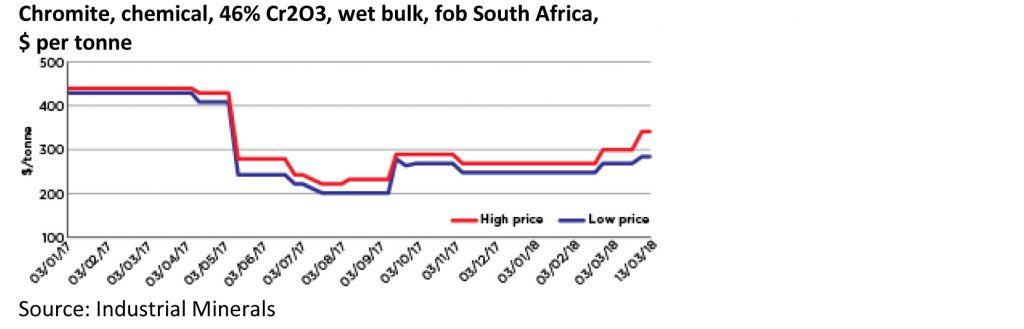

Chromite Prices rise further in chemical, foundry grade chromite markets Chromite prices have moved up further at the beginning of March with limited availability continuing to put pressure on supplies of both chemical- and foundry-grade material, while premiums are rising in some cases.

Demand for foundry sand remains high across the board, with major markets in western countries as well as Asia showing continued willingness to source material, market participants have told Industrial Minerals. This is exacerbating the limited availability of foundry material, after a number of operations closed in 2015-16 when market prices were low.

«Prices have recovered since that long period of weakness two-three years ago, but demand has surged. This is why you see prices ticking over on the spot market so much. Now, it’s evident that the market is undersupplied,» one distributor said.

The highest price pressure is being seen in dried and bagged material, which is the most common form of chromite used by refractories and foundry consumers. This is, again, essentially related to strong demand from various destinations, including Europe, North America, Southeast Asia and China.

As a consequence, the price of wet bulk foundry-grade chromite is also edging upward, albeit at an overall slower pace. The price of foundry-grade chromite, 46% Cr2O3, wet bulk, increased to $480-500 per tonne fob South Africa, from $450-470 per tonne, according to Industrial Minerals’ price assessment on March 6. Dried and bagged material, which normally commands a $50 premium over wet bulk, was reported to be selling at $550 per tonne and, in some cases, as much as $600 per tonne fob South Africa.

Changes were also seen in the prices for refractory-grade and lower-purity foundry material. The price of refractory-grade chromite, 46% Cr2O3, wet bulk, was $470-500 per tonne fob South Africa, compared with $440-470 per tonne previously. And the price of foundry-grade chromite, 45.8% Cr2O3, wet bulk, was $470-490 per tonne fob South Africa, against $440-460 per tonne previously.

Chemical-grade chromite The chemical chromite market is meanwhile showing a wider price spread than usual, on diverging drivers between contracting activity in China, which is the single largest buyer, and western markets. Suppliers in conversation with Industrial Minerals noted that western markets were accepting higher prices compared with China, where local buyers were still bidding much lower.

This has pushed prices upward in Europe and other western markets, while Chinese prices have lagged. The price of chemical-grade chromite, 46% Cr2O3, wet bulk, was assessed at $285-340 per tonne fob South Africa, marking a wider overall range compared with a previous level of $270-300 per tonne.

Industrial Minerals is aware of a number of deals for mid-sized parcels being made in western markets at the high end of the price range. At the same time, activity in China remains consistently at prices below the $300-per-tonne mark.

«Chinese customers are very aggressive right now; they just won’t give in to higher quotes,» one trader said. In some cases, premiums between metallurgical UG2 chrome ore and chemical grade were reported to be increasing against historical averages.

The Metal Bulletin index price for South African UG2 was $241 per tonne cif China on March 2. While the average premium for chemical grade over metallurgical would be $40-50 per tonne, in some cases this has increased to anywhere in the range of $80-100 per tonne.

«You can see that, for LG chemical material, where supply is tight compared with UG2 chemical, premiums are much higher than they used to be,» a supplier said. «We expect that to continue because of constrained supply.»

TiO2 Chinese

TiO2 producers cite yuan appreciation as they push for price rises Titanium dioxide producers in China are attempting to raise prices after coming back from the lunar new year holiday, citing a shifting exchange rate.

TiO2 prices are denominated in dollars, but the strengthening yuan is decreasing local-currency receipts for sellers. At the time of publication, the yuan was trading at 6.31 yuan to $1, down by about 8% year-on-year.

«They’re saying that due to the [yuan appreciation] they can make more money selling domestically,» one European trader told Industrial Minerals. «After Lomon [Billions] increased prices, every seller tried to follow suit.» Despite agreement that higher prices were being sought, buyers reported that they had not been seen in deals so far.

«We haven’t bought at the higher prices yet,» a European buyer told Industrial Minerals. «But they’re definitely going to keep trying to push prices up.» On March 1, Industrial Minerals assessed the price of titanium dioxide pigment, high quality, bulk volume, cfr Asia, unchanged week-on-week at $2,700-3,100 per tonne.

Titanium dioxide pigment, high quality, bulk volume, CFR Asia, $/tonne

DBM High-grade DBM prices leap on lack of raw materials Chinese prices for high-grade dead burned magnesia (DBM) edged up after the lunar new year holiday due to tight supply of high-quality magnesite ore while low-grade DBM prices drifted lower amid sporadic buying.

Following a series of state-mandated mining limitations in magnesia-producing areas across China, such as Liaoning and Heilongjiang, local producers continued to face challenges in securing sufficient raw magnesite ore for processing.

Spot prices reflected those challenges, with low availability pushing Industrial Minerals’ high-grade DBM prices up by as much as $300-500 per tonne. Still, weaker demand pressured low-grade prices lower.

The price of DBM 97.5% MgO lump increased to $1,100-1,400 per tonne fob China on March 9 from $630-740 per tonne a week earlier, while 94-95% MgO material rose to $680-700 per tonne fob China from $385-470 per tonne. Strict controls on magnesite, the raw material in the production of magnesia, are directly affecting plants’ ability to produce sufficient high-grade DBM, producers told Industrial Minerals.

«The government has maintained strict control over exploring magnesite this year and producers remain unable to use explosives to get high-quality raw materials,» a producer in Haicheng said. No dynamite blasting or pneumatic drilling is permitted at a large number of mines in Liaoning, a second source added.

Still, soft demand for low-grade DBM caused prices of 90% and 92% material to fall.

The price of DBM 90% MgO fell to $240-280 per tonne fob China on March 9 from $330-350 a week earlier, and 92% MgO fell to $280-300 from $350-390 per tonne. Fused magnesia (FM) prices also fell in China amid thin buying. The spot price of FM 97% MgO (Ca:Si 1:1) dropped to $1,150-1,250 per tonne fob China on Tuesday from $1,400-1,600 per tonne on February 27, and 97% MgO (Ca:Si 2:1) fell to $1,250-1,400 per tonne from $1,600-1,800 per tonne.

Caustic calcined magnesia (CCM) prices remained stable: the 94% MgO fob China price held at $240- 260 per tonne, 90-92% MgO at $205-230 per tonne and 96% MgO at $335-355 per tonne.

«China’s CCM market is quiet, with limited new deals concluded after the holiday. International consumers have started to seek magnesia suppliers outside of China since Chinese magnesia prices surged due to strict environment inspections last year.

I heard buyers purchased large volumes of CCM from producers in Brazil last year,» a trader in Dalian said. In the European market, prices remained firm while non-Chinese producers continue to report high demand both from ordinary customers and from those buyers which switched sourcing after failing to secure supply from China.

Several producers outside China claimed to have contracted almost all of their material for the first and second quarters of this year, leaving only small volumes for spot trading.

Industrial Minerals assessed the price of European CCM, agricultural grade, at €250-350 ($309-433) per tonne cif Europe, unchanged from February 27, and the high-grade FM price at $1,500-1,700 per tonne fob Europe was also unchanged.

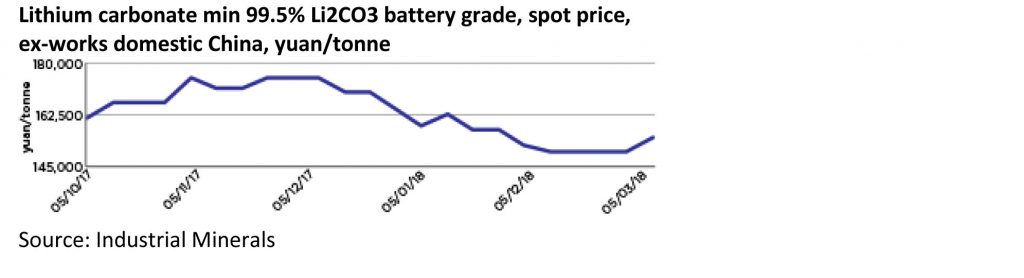

The price of raw magnesite remained at €65-80 per tonne fob East Mediterranean. Lithium Lithium prices rise in China after new year break Chinese lithium producers pushed prices higher this week on expectations of rising demand from the new energy vehicles (NEVs) sector, and some lithium-ion battery cathode material producers have started to replenish stockpiles on an as-needed basis after the lunar new year holiday.

The spot price for battery-grade lithium carbonate (min 99.5% Li2CO3) increased to 150,000-160,000 yuan ($23,771-25,356) per tonne* on March 8, from 145,000-155,000 yuan per tonne a week earlier, according to Ind-ustrial Minerals’ market assessment.

«The Chinese domestic battery-grade lithium carbonate spot market has gone up, with suppliers expecting more sales post-holiday. I think prices will stay at this higher level for a while. We plan to increase our offer price to 165,000 yuan per tonne later,» a lithium producer told Industrial Minerals. Meanwhile, prices of technical and industrial grade lithium carbonate and lithium hydroxide monohydrate have held steady this week on thin buying activity.

The spot price for lithium carbonate (min 99% Li2CO3), technical and industrial grades, ex-works China, was stable at 145,000-150,000 yuan per tonne on March 8.

The price of technical and industrial grades of lithium hydroxide monohydrate (min 56.5% LiOH.H2O) remained at 140,000-145,000 yuan per tonne, while the price of lithium hydroxide monohydrate battery-grade material was unchanged at 148,000-153,000 yuan per tonne on March 8. Seaborne markets The spot prices for seaborne China, Japan and South Korea lithium carbonate (Li2CO3) and hydroxide monohydrate (LiOH.H2O) stayed flat, with overseas buyers showing no interest in restocking.

The spot price for lithium carbonate (min 99% Li2CO3), technical and industrial grade, cif China, Japan and South Korea, remained at $17.50-19.50 per kg, according to Industrial Minerals’ market assessment on March 8. The spot price for lithium carbonate (min 99.5% Li2CO3) battery grade cif China, Japan and South Korea, was similarly stable at $19.00-21.00 per kg. The seaborne lithium hydroxide monohydrate (LiOH.H2O) market remained quiet, with buyers still negotiating prices with suppliers.

The prices for technical and industrial grades of lithium hydroxide monohydrate (min 56.5% LiOH.H2O) were unchanged at $19-21 per kg while the price for the battery grade* was $19-22 per kg, both on a cif China, Japan and South Korea basis on March 8.

Andalusite Persisting market tightness leads to higher andalusite prices in 2018 The andalusite market is set to experience further tightness in 2018 with high consumer demand said to be exceeding available supply, driving contract prices for the year upward.

Limited availability is expected to persist throughout 2018, following a shortage that became apparent last year, when production issues resulted in lower output in major andalusite-producing regions. As a consequence of that, and of continuing high levels of activity in the refractory raw materials space, almost all market participants active in andalusite which were canvassed by Industrial Minerals claimed that current demand will not be covered with available supplies this year.

«I am fully booked, and I imagine others will be as well,» one supplier said. He added that some quantities produced this year may be needed to cover any outstanding volumes from last year’s contracts. His expectation was to run at full capacity throughout most of this year.

«There are no free volumes out there for the taking. Large buyers made sure they contracted early on, and even small buyers should have all agreed their supplies,» a trader said. A second trader added: «If you need material now, you’re not in a great position.

It doesn’t matter if you pay more, there just isn’t enough material around at this stage.» The second trader added that he kept receiving inquiries from new customers, but he was unable to meet their needs. Driving demand for the mineral was an improved performance in the refractories end markets, due to rising steel output, and a widespread shortage affecting several other refractory raw materials, such as bauxite and alumina. Andalusite can be used as an alternative to calcined bauxite for some refractory applications.

With Chinese bauxite output being slashed last year following government-led inspections and shutdowns, some consumers tried to move toward andalusite in search of volumes and better pricing conditions.

This brought about a peak in demand in the andalusite space – a market that is much smaller and more stable than that for bauxite. Market participants claim that it will take some time before the supply/demand situation returns to normal. Shorter contracts, higher prices While andalusite is normally contracted with long-term, annual agreements, in a number of cases this year contracts were shortened to six months.

In other deals, volumes were agreed for the year although the price was fixed only for the first six months – leaving the possibility of reviewing the price for the second half of the year. Some large buyers reported that they managed to set year-long contracts for both volume and price.

«All factors were there to drive prices upward this year, although we should bear in mind that any movement in andalusite is going to remain quite moderate,» a second supplier said. «You are not going to see a surge similar to what we saw in [refractory grade] magnesia.»

At the time of the UniteCR conference in Chile last September, sources in contact with Industrial Minerals were already suggesting price growth was in the offing once contracts came up for renewal.

Industrial Minerals assessed the price of andalusite, min. 57% Al2O3, at €260-320 ($322-396) per tonne fob South Africa for 2018 contracts, compared with €240-290 per tonne last year. While on the delivered Europe market, new contract prices for andalusite, min. 57% Al2O3, increased to €390-430 per tonne cif Europe, from €355-425 per tonne a year ago. Both market prices have shown a rise of about 10% from previous levels, which is in line with earlier forecasts from market participants, who pointed to an appreciation ranging from a low of 5% – for those buying particularly large quantities or managing to secure preferential conditions – to a high end of 15% for smaller purchasers or new customers.

«Your 2018 price would also depend on what kind of price you had last year. If your 2017 price was on the low end of the range, the increase may be higher. If it was on the high end [of the price range], the increase would be small,» a third trader source said.

A third supplier added: «All my selling prices have gone up this year – by different amounts, of course.» Some market sources suggested that currency volatility may also have an effect on market prices, considering that the US dollar is going through a particularly weak phase and the South African rand has appreciated strongly in recent weeks. But the timing and length of contractual patterns do not support this view, because all contracts set during the final quarter of last year and the early stages of this quarter would have locked in a price level for either six or 12 months ahead, thus excluding any currency exchange effect for the time being. If any deals were to be updated in the second half, currency effects may be factored in at that point.

Celesite PRICING NOTICE: Extension of consultation period for proposal to discontinue celestite price During the initial consultation period, which ended Wednesday February 28, Industrial Minerals received feedback from the market that indicates the need for further engagement on the proposal regarding the discontinuation of the following prices: Celestite, Turkish, 96%, SrSO4, fob Iskenderun, $/tonne The extended consultation period will end one month from the date of this pricing notice, on April 13. To provide feedback on this price or if you would like to provide price information by becoming a data submitter, please contact Industrial Minerals by email at: pricing@indmin.com. Please add the subject heading re: Celestite Please note Industrial Minerals reserves the right to refine these prices if sufficient market demand warrants such action.

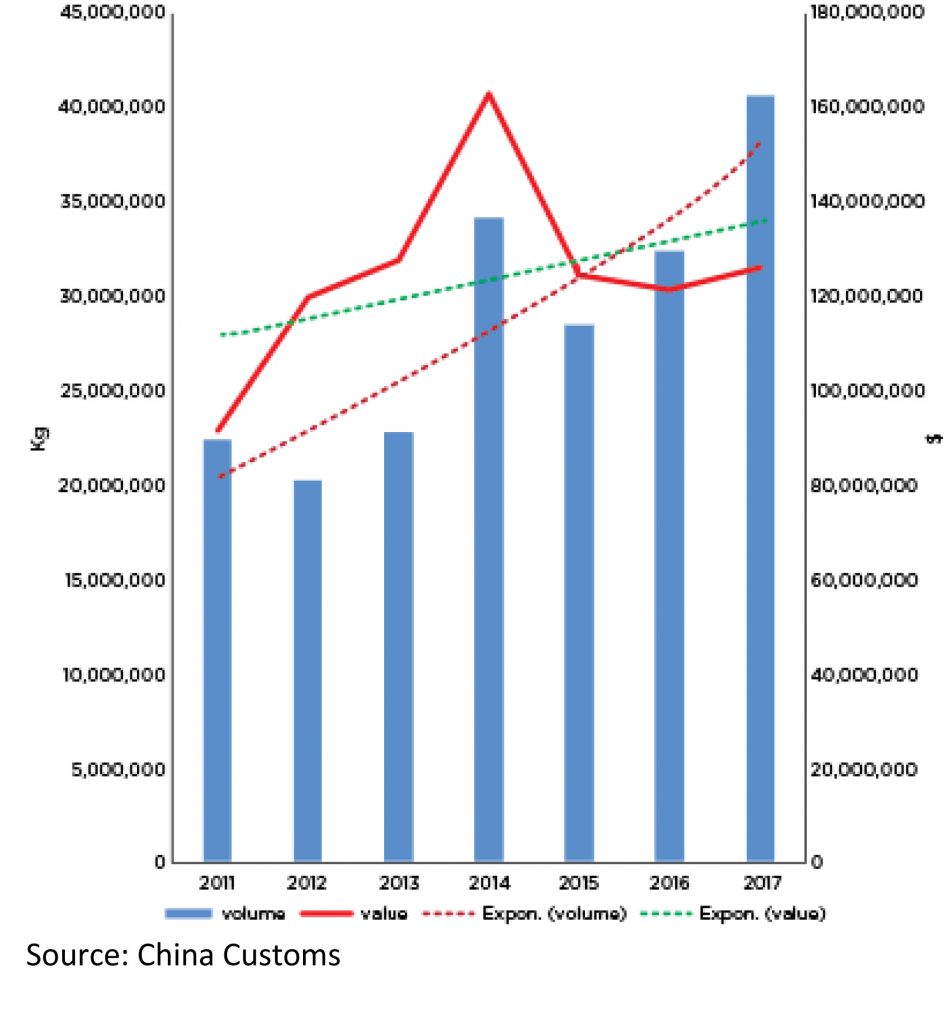

To see all Industrial Minerals’ pricing methodology and specification documents go to www.indmin.com/Methodology. Spherical graphite Chinese spherical graphite exports at seven-year high on surging EV demand Chinese exports of spherical graphite (SG) reached a seven-year high in 2017 and demand has continued to rise into this year, with a surge in January consignments, the latest customs data shows. Exports of spherical graphite, including uncoated and coated material, rose last year to 40,871 tonnes, up by 25% over the previous year.

The 2017 total was also the highest since at least 2011, when Industrial Minerals’ records begin. The increase followed rapid growth in battery end-markets, which reflected ambitious targets for production and sales of electric vehicles (EVs) among major carmakers in leading markets including China and Europe. China will produce more than 1 million new EVs domestically in 2018, further supporting demand for raw materials such as lithium, cobalt and graphite. The uptrend in SG trading continued into early 2018. Exports of SG in January this year surged to 5,238 tonnes, with a value of $15.77 million.

This was up year-on-year by 92% in volume terms and by 71% in value. In value terms, however, the performance was mixed. While the total value in 2017 of $126.55 million was 3% higher than the $122.16 million of the previous year, the rate of growth essentially reflected the higher export volumes. But the average unit value of the material declined. The average unit price was $3,096 per tonne, according to figures from Chinese customs, a drop of 17% from the average of $3,748 per tonne in 2016. In previous years, unit values were higher despite lower overall volumes being traded.

This suggests a persistence of the supply/demand imbalance that, over the past few years, has characterized the SG market, which has also been dogged by overcapacity.

Chinese regional governments had been encouraging widespread production of both uncoated and coated spherical material from local companies to serve the battery sector. This encouraged the domestic graphite industry, which is fragmented and dominated by small firms, to seek in greater numbers to benefit from tax breaks and favorable conditions.

But demand from battery makers had not increased as rapidly, leading to a supply of material that end-markets could not absorb. In turn, this brought about a progressive decrease in SG prices. The latest decline in graphite export values in the customs data shows how this remains a determining factor.

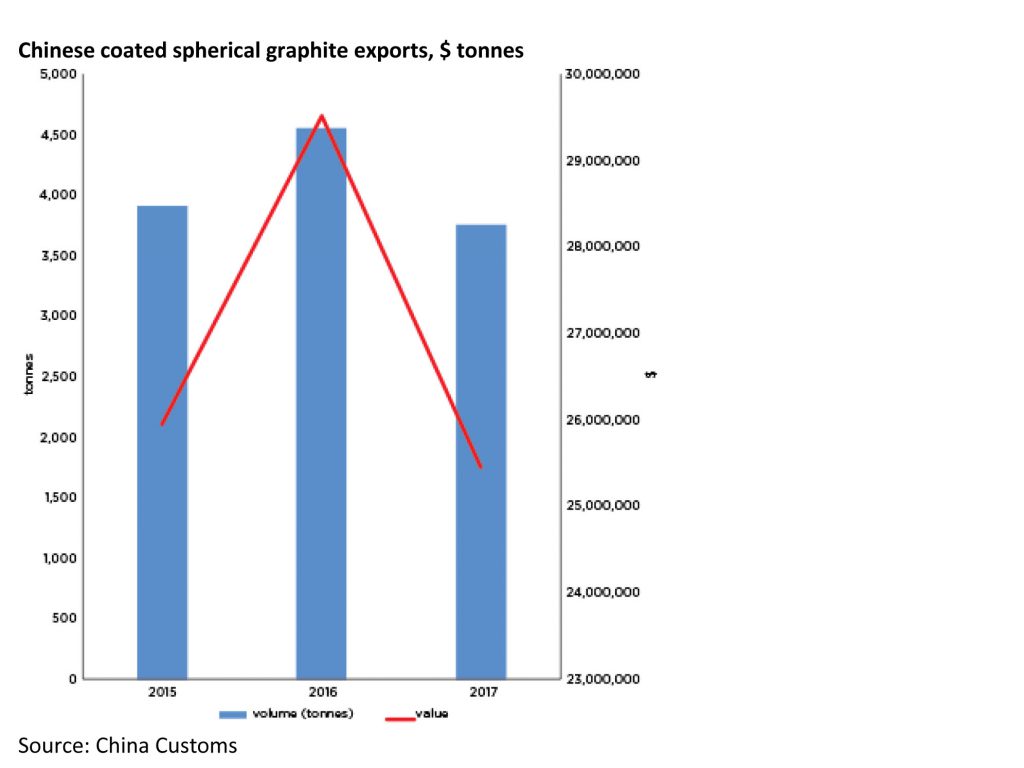

Prices have, similarly, been sluggish. Industrial Minerals assessed the price of Chinese uncoated spherical graphite, 99.95% C, 15 microns, at $2,250-2,700 per tonne fob China on March 1, compared with $2,500-3,000 per tonne in January last year. Coated SG declines While total exports ended the year on a high, the performance of Chinese coated SG told a different story.

Total exports of this material (HS code 38019010) were 3,805 tonnes last year, not only down by 17% from 4,609 tonnes in 2016 but also down from 3,976 tonnes in 2015. In value terms, 2017 exports generated $25.49 million, a 14% drop from $29.62 million in 2016 and also down from $25.99 million in 2015. China mainly sells SG in its uncoated form to other destinations in Southeast Asia, such as Japan, where the coating is applied. Chinese exports of coated SG are, in comparison, much lower.

Graphite remains the primary component of the lithium battery anode in the mainstream battery chemistries (LMO, LFP, NCM, NCA) in use today. It can also be found in small volumes in the cathode to enhance conductivity.